April 2020

The wider impacts of COVID-19 are still very much ahead of us, and with it many unknowns. In recent weeks I have had plenty of conversations with my clients and other property professional as to where the property market in London is now, and where it is heading with Coronavirus. Below are some observations and opinions following these discussions.

PRIME LONDON Q4 2019 – Q1 2020

2020 began with the wind in our favour following a positive end to 2019. In the run up to and following the Conservatives comfortable victory in December’s UK General Election, the property market saw a real boost in activity across Prime London. Competition and much needed confidence returned to the market which transpired into positive results on transaction numbers and values.

Prices were up by 6.6% on the previous 12 months with a staggering 6.1% of this coming from Q4 2019 and Q1 2020. According to Zoopla, agreed Sales at the beginning of the year were also up somewhere between 5-10% in the first quarter when compared to the same period in 2019.

The numbers looked very promising before the Coronavirus Pandemic reared its head.

CORONAVIRUS UK LOCKDOWN

The Coronavirus Pandemic resulted in the UK Government announcing a lockdown in late March. The UK property market esssentially came to a grinding halt… Most estate agents closed their doors to the public, viewings stopped and the existing pipeline of agreed sales were either put on hold or simply fell through.

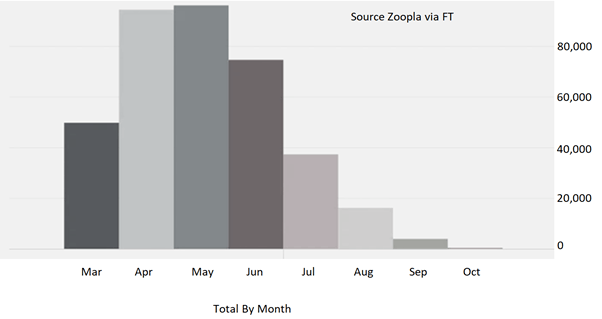

The below graph shows the number of estimated Property Sales in the UK which were put on hold since Coronavirus restrictions came into place in March.

According to Zoopla, around 300,000 transactions are currently on hold. This accounts for approximately £82 Billion is sales values. In normal times, these transactions would theoretically, be completing between April and June this year.

To put the graph in perspective, Zoopla suggests in a normal market that around 270,000 sales are in the conveyancing process, with approximately 100,000 completed each month.

Some of the agreed sales put on hold will transact eventually but a great number will simply fall away, and its safe to say that the longer the lockdown lasts, the greater the number of fall throughs will occur.

MORTGAGE LENDING PRACTICE

Mortgage lenders have a big part to play in the levels of transactions during this time. Many have already extended existing offers by a further three months to borrowers who were unable to complete due to the lockdown measures.

Following the ban on physical valuations of occupied homes by the government, lenders have also allowed people with lower deposits to still obtain mortgages through automated/desktop valuations.

The longer the lockdown measures stay in place, it is inevitable that lenders will start to reconsider their offerings. Many have already reduced their maximum loan to value (LTV) ratio which immediately reduces the amount of risk they are willing to take on.

QUICK REBOUND POSSIBLE IF LOCKDOWN ENDS IN TIME FOR SUMMER

When Covid-19 recedes, and normality returns, I believe the property market will start moving again pretty quickly. But why?

Political Certainty – I believe the same reasons the property market revived towards the end of 2019 and the beginning of 2020 still exist now, even if currently dormant. A great deal of uncertainty was removed following the results of the UK Election and with it came an instant increase in market demand shown through an uplift in prices and transactions. If we can have an effective lockdown strategy with property transactions getting back to (close to) normal levels this summer, we could see the market continue on from where it left off.

Weak Sterling – The pound remains at a historical low, which will continue to attract overseas investors. This along with the proposed 2% increase in stamp duty deadline (coming into play in April 2021) could create some real urgency in the marketplace, and possibly aid in a faster than normal rebound for Prime London property.

Interest Rates – Money is cheap! Interest rates are at a historic low and look to remain so for a while. This crisis is quite different to the 2008 global financial crisis. This is not a credit crisis; borrowers are not at risk of been over extended. The banks learned their lesson on the affordability of its products, and as such will keep lending!

Finally, I would like to express my sympathies for everyone who has been affected by Coronavirus. I would also like to thank the NHS and all Key workers who continue to face this horrific virus head on, for the rest of us. We truly are in this together and will get through it.

For more information on the above article, please contact info@xanderprime.co.uk and for full details of what services Xander Prime offers, please visit www.xanderprime.co.uk

Best regards and stay safe

Alexander Wall

Previous Article Next Article